Truflation US Inflation Update for February 2025

Published 11 Mar, 2025

Executive Summary

President Trump has pledged to unshackle the economy, but his trade policies, especially the tariffs on key trading partners like Canada, Mexico, and China, have sparked concerns about the future of economic growth. These tariffs challenge the framework of globalized trade, which has been a cornerstone of U.S. economic expansion for decades.

The tariffs mean that American consumers are facing higher price, especially on everyday items like vegetables, wheat, toys, and t-shirts, which are particularly burdensome for consumers, who have already faced a relatively high level of inflation. The imposition of these tariffs will likely add between 0.5% to 1.0% on the current inflation rate. This would compound existing inflationary pressures, making goods more expensive for American consumers. In addition to this Trump’s policies on immigration could exacerbate the problem, potentially leading to a stagflationary shock.

The sentiment within the manufacturing sector is weakening, signalling potential concerns about future growth. This may be due to the uncertainty caused by tariffs, trade disruptions, and the broader economic climate. The recent trade deficit has increased significantly, in part due to businesses stockpiling goods in anticipation of tariffs.

At the same time, there are cuts to the federal workforce and reductions in government spending. This may further slow economic activity, as public sector cuts typically reduce overall demand for goods and services in the economy. Tightening of immigration policies is creating concerns about labor shortages, especially for industries that rely on immigrant workers.

Given all these factors, investors are now predicting that the Federal Reserve will lower interest rates by about three-quarters of a point by the end of 2025. However the expectations of the upcoming meeting on March 19th is that interest rates will remain unchanged. Policymakers will be looking for more trends in the data before making any major changes in the short term.

- Personal spending fell by 0.2% from December to January, marking the largest drop since early 2021. Retail sales also saw a larger-than-expected decline, indicating that consumers are becoming more cautious with their spending.

- Steep decline in consumer confidence which was significantly worse than anticipated, signalling that consumers are more uncertain about the economy.

- Drop in construction spending by 0.2% between December and January, adding to concerns about economic activity in sectors tied to physical infrastructure and housing.

- Carmakers' vulnerability to the ongoing trade tensions, with car manufacturers facing a potential 25% tariff increase. Although these tariffs have been delayed by a month, the threat still looms, creating uncertainty and potential cost increases for carmakers and consumers.

- The Department of Government Efficiency is set to implement measures aimed at reducing the fiscal deficit, which could involve slashing government jobs and reducing spending. These cuts could further dampen economic activity, as government spending is an important component of overall demand in the economy.

It is still too early to determine the impact of recent economic developments on first-quarter GDP growth but a Bloomberg survey suggests a reasonably strong annualized growth rate in Q1 of 2.2%, just slightly slower than the official 2.3% reading from Q4. However, the Atlanta Federal Reserve’s forecast has taken a significant downturn, dropping to -2.4%. This sharp revision is largely due to the surge in the U.S. trade deficit but the Atlanta Fed expects its model to strengthen once more February data becomes available.

Despite these concerns, there are still signs of strength in the economy. Personal income grew by 0.9% between December and January, which is a positive sign of economic health. This growth pushed the savings rate up to 4.6%. The private sector data revealed a pick-up in commercial bank lending for consumer credit in recent weeks, suggesting that despite broader concerns, some segments of the economy are continuing to perform well. Overall, economists still expect a relatively positive economic performance for the year, though there are mounting threats that could derail this outlook.

Recent inflation trends

Inflation continues to remain as a top concern for the US Economy not only given the recent developments with regards to tariffs, which are likely to impact the cost of goods but also driven by the tight labor market and its implications on the cost of services. If the economic growth stutters in the short term we could be seeing signs of stagflation returning.

According to the BLS, annualised inflation surprisingly continued to rise in January, despite the festive season coming to an end, which was opposite to what Truflation was reporting. This downward trajectory as highlighted by Truflation in January is expected to continue in February.

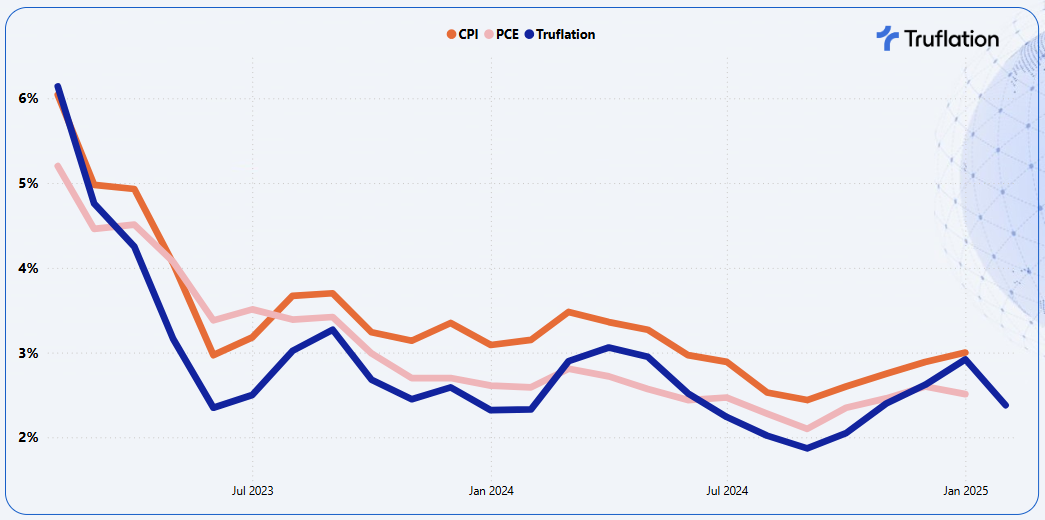

Exhibit 1 –Annualised Inflation Comparison: Truflation, PCE and CPI vs 2% Federal Reserve Target

Truflation is forecasting a continued decline in CPI reading for February, with a annualised increase of 2.8% from January 3.0% YoY. This projection aligns very closely with the broader market expectations, which ranges from 2.8% to 3.0%.

It is core inflation that is the driving force with gradual moderation in the more volatile categories of food and energy which have held up more significantly. The secondary driver in inflation this month is consumers expected to take advantage of lower prices as inventory needs to be flushed out as well consumer taking advantage of lower costs before the up and coming hikes in the cost of goods as a result of the tariffs.

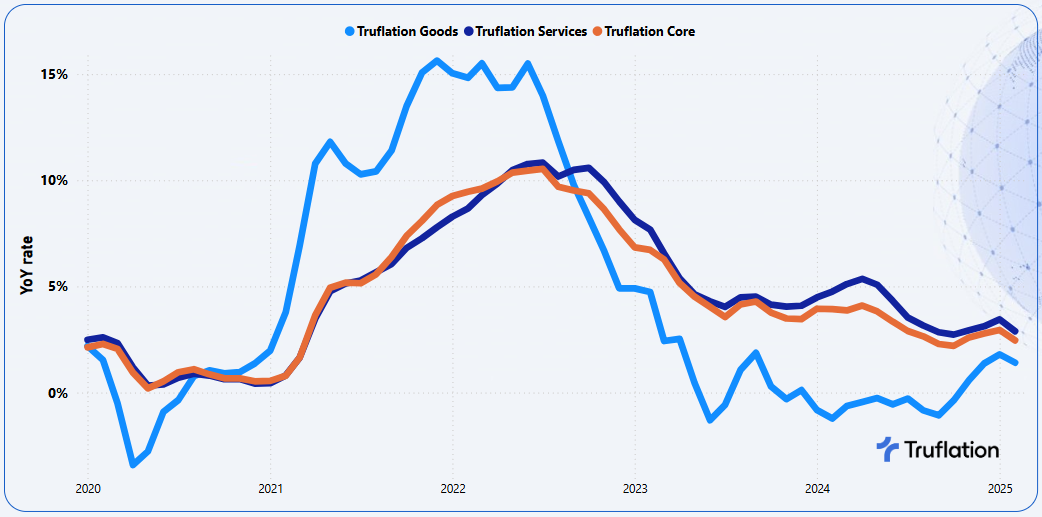

Exhibit 2 – Truflation key inflationary metrics: Goods vs Services vs Core Inflation

Given the current economic predicament, it suggests that the Federal Reserve may need to tread cautiously in its policy decisions as we look ahead into 2025, at least until inflation shows more consistent signs of retreat. The markets are now expecting three rate hike drops this year totalling 75 basis points.

Exhibit 3 – Truflation key inflationary metrics: Goods vs Services vs Core Inflation

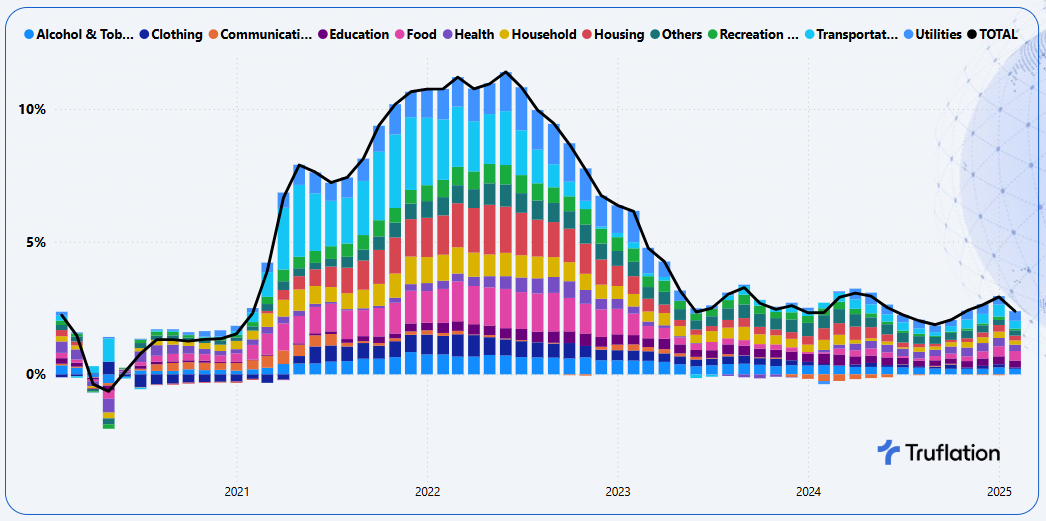

The most significant upward contributions to inflation in February came from food, housing and utilities while transportation and alcohol & tobacco were the biggest downward contributors.

Sector-Specific Inflation Analysis

- Food: Prices rose +0.9% MoM and +3.9% YoY and was driven by both food at home as well as food away from home. As much as this is driven by supply chain disruptions and extreme weather conditions prices of goods eg eggs, commodities etc have increased coupled the continued strong wage growth.

- Housing: Overall housing prices rose +0.5% MoM and +2.0% YoY. However, it is the owned housing seeing a growth of +0.6% MoM and +2.9% YoY. Home sales haven’t started off the year well with existing home sales falling 4.9% in February likely due to mortgage rates refusing to budge for several months despite interest rate cuts last year. Prices are up 4.8% from a year ago and has accelerated. Housing inventory is up 3.5% with unsold inventory now standing at 3.5 month supply up from 3.2 months. More supply allows for more strongly qualified buyers to enter the market but to drive sales significantly lower mortgage rates and more supply are necessary. Rented housing, on the other hand, was relatively stagnant +0.1% MoM and +0.6% YoY. The other factor in the Housing segment is Other Lodgings that include Hotels and Airbnb etc, which has rebounded from January drop as a result of an increase in business travel.

- Utilities: Prices rose +0.8% MoM and +3.9% YoY as a result of the extended cold blast with Winter expected to last until early March.

- Transportation: Prices saw a notable drop in the rate of increase to -0.1% MoM and +3.3% YoY with the single biggest driver being vehicle purchases, as dealers look to shift volume with lower price points.

- Alcohol & Tobacco: Prices accelerated their deflation trajectory with a -0.5% MoM and +2.3% YoY, driven by alcoholic beverages as Americans return back to their normal buying behavior and continuing back to their healthier living.

- Recreation & Culture: +0.0% MoM and +0.7% YoY is driven by consumers being more selective and prioritizing their spend. A recent study by PwC highlighted that 34% of the consumers were cutting back on events and outings allowing them to indulge where it matters most to them.

Longer term outlook

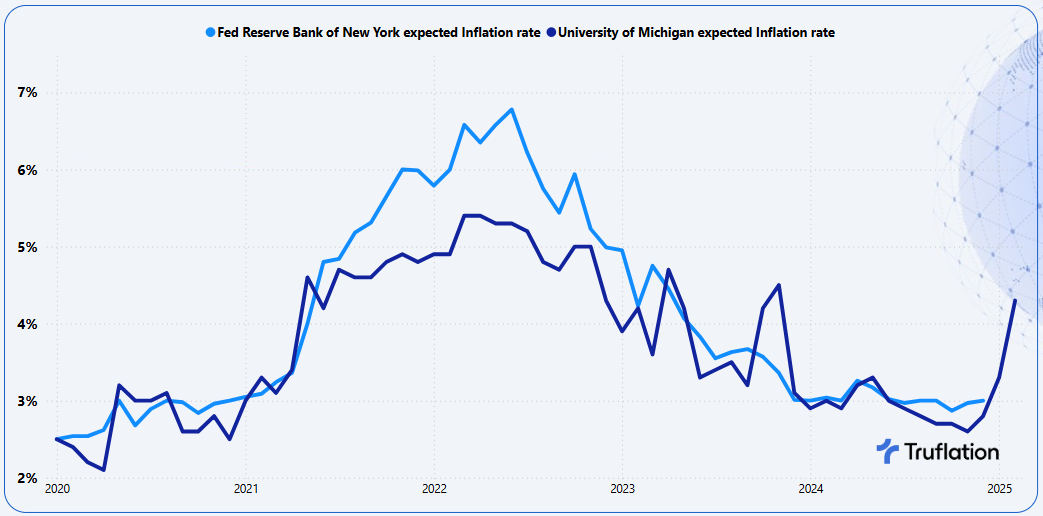

The signs for the road ahead continue to be bumpy with more upward inflationary pressures. These fears of higher prices from tariffs have sent consumer 12 month inflation expectation soaring to more than one year high in February, the survey from university of Michigan showed.

Exhibit 4 – Consumer Inflation Expectations (2% is the Fed Target)

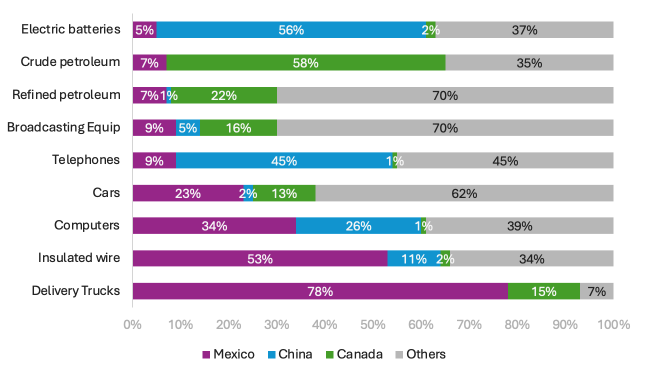

The impact of tariffs on Mexico, Canada, China as well as tariffs on steel, will most likely be passed on to the consumer in some shape. The likely key categories to be impacted are:

- Automotive: Prices are likely to increase by about $3,000, according to TD Economics, which is a result of parts crossing the US, Canadian and Mexican borders multiple times before a vehicle is assembled. This especially impacts Audi, BMW, Ford, General Motors and Honda. Disrupting these trends through tariffs would come with significant costs.

- Fuel prices: Canada is America’s largest foreign supplier of crude oil with 61% of Oil imported into the US between January and November 2024 coming from Canada. The US doesn't have a shortage of oil, but the type its refineries are designed to process means it depends on heavier ie thicker crude oil which mostly comes from Canada and some from Mexico. These are needed to maximize flexibility of gasoline, diesel and jet fuel production.

- Housing: US imports about a 1/3 of its softwood lumber from Canada which is a key building material and would push the housing affordability further out of reach for many 1st time buyers. Couple this with the steel tariffs (construction industry is the single biggest user of steel) which could result in developers pushing out the building of new homes, creating less inventory on the market and again pushing prices up further. On the 1st of March President Trump ordered an investigation into whether the US should either place additional tariffs on most lumber and timber imports, regardless of their country of origin, or create incentives to boost domestic production. Findings are due towards the end of the year.

- Maple Syrup: Canada's billion-dollar maple syrup industry accounts for 75% of the world's entire maple syrup production with 90% produced in Quebec. Consumer might choose to buy goods that are domestically produced in the US, but they are produced using inputs from Canada, thus will also see prices rise.

- Avocado’s: They are primarily grown in Mexico due to its warm, humid climate and Mexican avocados make up 90% of the US avocado market.

- Canned food & Carbonated Soft Drinks: Roughly 70% of the steel used in the US to make cans for food is imported today coming mainly from Germany, Netherlands and Canada and is currently not produced in the US. This combined with the impact of Aluminium will likely drive up grocery prices for canned foods made in the US.

- Beer Whisky & Tequila: The most popular beer brand in the US is the Mexican Modelo with a strong cult following of Corona and the tariffs could result in more expensive products for the US customers if the companies importing them pass on the increased import taxes. In terms of spirits its more complicated with certain brands of Tequila and Canadian Whisky being recognized as distinctive products and can only be produced in their designated countries. Given the production of these drinks can’t simply be moved, supplies might be impacted, leading to price rises.

Exhibit 5: Which products will be affected by Trump Tariffs? Key items imported to the US from Mexico, China and Canada in 2024.

You combine the tariffs and its associated impact on Inflation with immigration policies and the employment market we can likely see more inflationary pressures on goods as well as services. Not only is this story is that the impact of tariffs but is this also going to impact economic growth.

Conclusion

In the short to medium term, we are going to have a couple of one-time adjustments to inflation with the question of how resilient the consumer remains supporting growing with increased indicators that should be at a minimum a note of caution.

APPENDIX A

Truflation Category Percentage Change Data

Month-over-Month and Year-over-Year

All Data is based on February 2025

About Truflation

Truflation provides a set of independent inflation indexes drawing on 60+ data partners/sources and more than 30 million product prices across the US. These indexes are released daily, making it one of the most up-to-date and comprehensive inflation measurement tools in the world. Truflation has been leveraging this measurement tool to predict the BLS CPI number with remarkable accuracy. We have successfully predicted the number with precision in 6 of the last 8 months. In 2024, our forecasts had an average deviation of just 0.06%.

Truflation Website | TRUF.Network | X | Linkedin | Discord | Telegram | Github| YouTube

Truflation

Privacy Policy | © 2025. Truflation - All Rights Reserved.