Truflation: US Inflation Update January 2024

Published 12 Feb, 2024

Consumer spending remains strong in a tight labor market

On January 25, the Bureau of Economic Analysis (BEA) released its advance estimate of GDP growth for Q4 2023, which came in at 3.3% – significantly higher than the previously expected 2%. On top of this, the US consumer remains extremely resilient, defying market expectations.

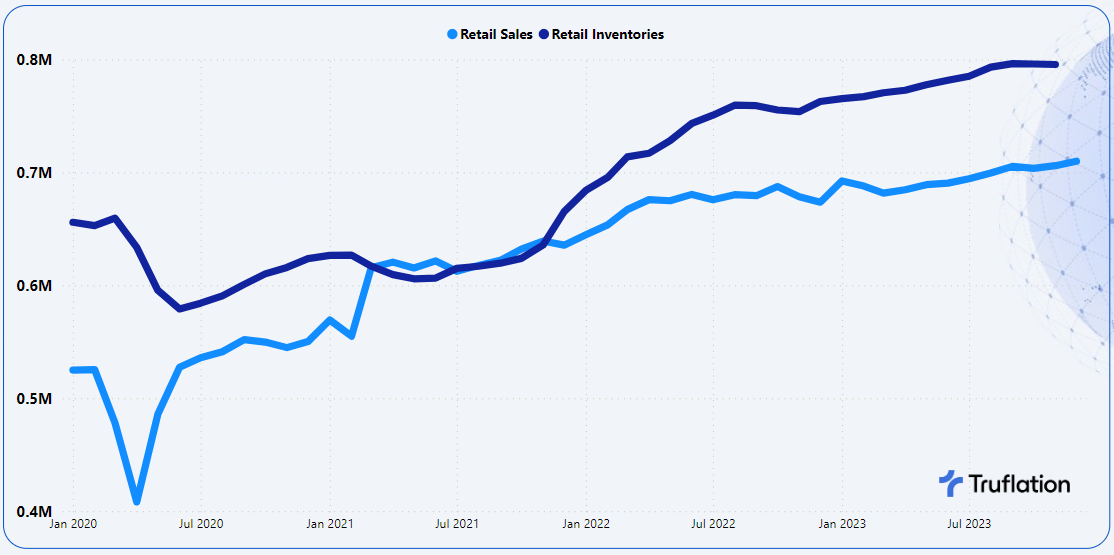

In particular, spending remained strong in December as a result of the festive season. Retail sales increased 0.6% month-over-month (MoM) and 5.4% year-over-year (YoY). This figure marked an acceleration from November’s 0.3% MoM growth and beat economists’ estimates of 0.4%, driven primarily by clothing, accessories, and online sales.

Graph 1: Monthly Retail Sales and Inventories - Adjusted

Source: US Census Department; Advance Monthly Retail Trade Survey

The sales gains were broad-based and indicate that consumers are keeping up with price increases in the market. This rampant consumer spending certainly adds complexity to the Federal Reserve’s monetary policy decision at the next meeting in March.

At the same time, inventory levels have peaked and started to see a slight decline. However, this was somewhat offset by the continued growth in inventory levels of motor vehicles and parts dealers, suggesting that we are likely to see further downward pressure on vehicle prices, even as inventory levels drop in other sectors.

With consumer spending still on the rise, how is this being funded? For one part, it appears consumers are still borrowing to fuel their spending patterns, especially on their credit cards. Household debt has hit a new record, up 3.6% YoY and 1.2% quarter-over-quarter (QoQ) at $17.503 trillion. Since 2011, all debt categories have been steadily rising. Credit card debt is a key component of this, increasing by $50 billion (14.5% YoY and 4.6% QoQ), now standing at $1.129 trillion.