Truflation: US Inflation Update March 2024

Published 08 Apr, 2024

Recent Inflation Trends

Inflation has not been cooling and in fact has seen a reversal of trends. In March, this upward movement is expected to continue and reinforce the Truflation position of continued sticky inflation.

Sticky inflation has been consistently reported by both the PCE and BLS. However, most recently, the Purchasing Managers Index (PMI) has reinforced the outlook that this is likely to continue and be driven by consumer demand. The PMI highlights that economic activity in the manufacturing sector expanded in March after contracting for 16 consecutive months.

The March PMI number registered 50.3%, up 3.5 percentage points from the 47.8% recorded in February. New orders moved back into expansion territory, backlogs contracting, production expanding and exports/imports growing. This has led to prices finally increasing.

This first instance of expansion since September 2022 shows that demand is likely at the early stages of recovery with clear signs of improving conditions for the manufacturing industry. Performance continues to defy projections for a downturn in activity and, with demand currently strong, we expect to see orders and production pick up in the second quarter.

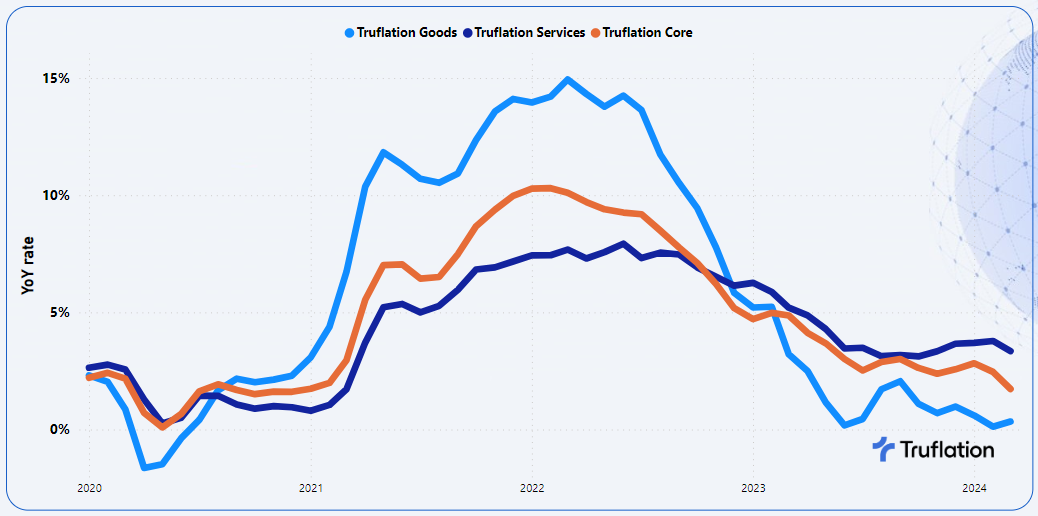

This will no doubt continue to fuel growth in the prices of goods (which includes food) now and in the future. Coupled with prices of services holding relatively stable in March, it is going to be tough to bring inflation down to the Fed’s 2% target.

Strong wage growth continues with employment opportunities being healthy and initial unemployment claims holding relatively stable. This strength in the employment market is likely to keep the cost of services stubborn for some time and will remain at the heart of the Fed’s fight against inflation.

Graph 1 – Truflation Core Inflation Measures (Core, Goods vs Services)

Read the full report here.

Want to be part of the data revolution? Join our Telegram to always be in the loop!