Truflation: US Inflation Update October 2024

Published 11 Nov, 2024

Executive Summary

The economy grew at a healthy rate, with the 1st estimate coming in at 2.8%, slightly down from 3% in Q2, driven by strong consumer spending despite the weight of the still high interest rates. Consumer spending, which accounts for 70% of the US economic activity, accelerated to 3.7% in Q3 up from 2.8% in Q2. Exports also grew 8.9% in Q3, however business investment slowed sharply due to reduced investment in housing and non-residential buildings. Despite widespread predictions that the economy would succumb to a recession, it has kept growing, with employers still hiring and consumers still spending. The latest data sends a clear message that the economy continues to reflect healthy durability.

Based on the latest data:

- PCE Price Index: The Federal Reserve’s favoured inflation gauge, the PCE, rose 2.1% year over year in September down from 2.3% in August, suggesting moderating inflation and within its range of 1.5% - 2.5%.

- Consumer Confidence: Truflation’s Consumer Confidence posted the biggest monthly gains since the beginning of the year. The Conference Board noted that the proportion of consumers who expect a recession in the next 12 months dropped to its lowest point since it started tracking this in July 2022.

- Job Market: There is a slight loss of momentum in the job market, with job openings falling (7.4 million from 7.9 million in August) to its lowest level since January 2021. Layoffs have risen combined with a drop in people quitting. Nonfarm payrolls were virtually unchanged in October (+12,000), following an average monthly gain of 194,000 over the past 12 months. The impact of the Hurricanes Helene and Milton combined with the strikes at Boeing and elsewhere had the effect of pushing down net job growth by tens of thousands of jobs in October.

- Wages: Average hourly earnings increased by 0.4% from September to October, with a 6.3% increase year-over-year. Union salary disputes, such as the recently resolved Boeing dispute, will contribute to wage growth.

- Federal Reserve Action: The Fed was satisfied enough with its progress against inflation and the slowing job market, that it cut its benchmark rate by 50 basis points. This signals an effort to balance inflation control with economic growth. The central bank’s policymakers have signalled another quarter-point rate cut this year, four more rate cuts in 2025 and two in 2026.

The cumulative result of the Fed’s rate cuts, over time, will likely be lower borrowing rates for consumers and businesses and drive demand based inflation.

Labor market trends

The Labor Department announced the unemployment rate remained at 4.1%. This suggests that while the labor market may not be as healthy as earlier in the year it is still fundamentally healthy.

The October JOLT report saw the addition of 12,000 jobs, a significant drop from the 223,000 jobs added in September. This decline is largely attributed to the impacts of Hurricanes Helene and Milton as well as strikes at Boeing and other locations, which collectively reduced net job growth by tens of thousands. Sectors such as healthcare and government were key contributors, adding 51,300 and 40,000 jobs month on month, respectively in October (seasonally adjusted).

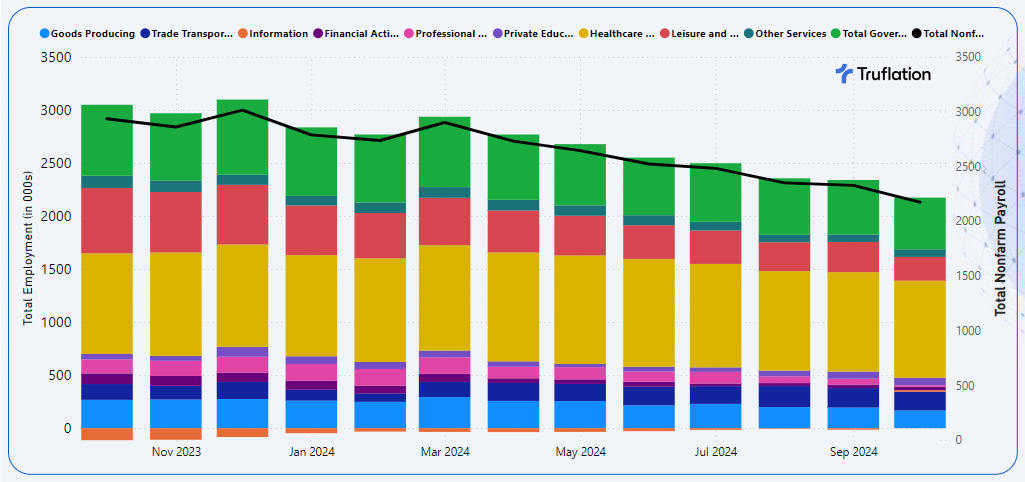

Exhibit 1 - Employee difference by sector compared to a year ago (seasonally adjusted)

Source: Department of Labor, Non farm payroll employment, Establishment Survey Data

Despite the continued additions to the job market, although at a slower pace, there is a cautionary sign for future hiring as temporary help services placement dropped 49,000 jobs last month and has decreased 577,000 since its peak in March 2022. This however is likely to only be a fraction of the total temporary employment. The election campaigns will also have a significant impact on the temporary job market in November, given that the election has now been concluded.

Initial Jobless Claims unexpectedly fell last week in a sign that turnover in the labor market remains low, but there is some evidence that employers have simply paused most of their personnel decisions until they can get a grip on a couple of macro-economic factors, especially given the recent rate cuts and the anticipated rate cuts in the future.

We have certainly seen the impact of AI, as 40% of the S&P 500 in their quarterly earnings reported to have said they are leveraging AI to drive productivity and sales. Those companies as an aggregate have experienced 12.5% gain vs those not talking about AI only seeing an 8.5% gain. Until we see AI deployed at scale, it is very likely we are going to see a continued pattern of job replacement and a tight labor market.

Recent inflation trends

Despite the progress made on inflation throughout the last couple months, average prices still far exceed their pre-pandemic levels, which has exasperated many Americans. The September annual rate as posted by the Bureau of Labor Statistics, was 2.4% which has come down considerably from the beginning of the year. Although, since the middle of September, Truflation has been reporting a reversal of this trend with a continued influence by housing, utilities, clothing, food and education.

Truflation’s forecast for the BLS CPI number for October, is an increase from September to 2.5% year-over-year (YoY) CPI for October, highlighting the acceleration. This forecast aligns closely with the market expectations, which ranges between 2.4% and 2.6%. This reversal of trends is being driven by core, and of course, the continued impact of services.

Exhibit 2 – Truflation key inflationary metrics: Goods vs Services vs Core Inflation

Beyond the macro-economic factors, inflation will continue to be affected by the tight labor market and the supply-chain constraints, which has been a persistent problem. With the recent Republican party win for the Presidential, Senate and House elections we are likely to see greater focus on protectionist trade policies and tax reductions, which will drive inflation further upwards. The geopolitical tensions will also play a significant factor that could influence inflation trends and directly affect transportation and production costs.

Sector-Specific Inflation Analysis

- Clothing & Footwear: This sector experienced a notable 2.7% increase MoM and 2.1% YoY, attributed to rising costs of commodities, labor and the new season’s collections hitting stores and driving sales.

- Utilities: Prices increased 0.2% MoM and 3.0% YoY, driven by higher costs for electricity, natural gas, and water. The contributing factor to this rise, is the elevated demand for electricity coming into fall, when temperatures are dropping.

- Education: This category experienced an increase of 0.5% MoM and 2.5% YoY. The driver of is the continued follow through of wage increases negotiated by the union that came into effect earlier this year, combined with the investments to keep up with market demand.

- Housing: Overall housing costs increased by 0.2% MoM and 1.1% YoY. However, the housing market shows mixed signals, with home sales declining month-over-month and median prices increasing month on month. The recent surge in mortgage rates back up to 6.7% at the end of October, has no doubt been hindering home sales, but factors usually associated with higher home sales are developing. There is more inventory choice for consumers, continued addition to the job market, and expected mortgage rate reductions, following the rate reductions and election outcomes. The other category driving prices upwards is hotels which have been climbing due to the return of corporate travel, but also heightened demand linked to the election season.

- Food & Non-Alcoholic Beverages: Prices rose 0.1% MoM and 2.2% YoY, driven by increased labor costs. Trends in out-of-home dining have seen the biggest driver behind the food increases, especially breakfast items.

- Transportation: Costs fell by 0.2% MoM but rose 2.9% YoY. Marginal increases in vehicle purchases have been offset by the declining gas prices, a result of lower crude oil costs.

Longer term views

The latest data from Truflation indicates an upward trend in inflation and this is expected to continue throughout the remaining months of 2024, driven by the persistent healthy economy that will fuel demand based inflation.

Beyond this, with the election results we can expect further inflationary pressures given the promises from the campaign trail. These factors include:

- Inflation Reduction Act: There are expected changes in both the administrative and legislative elements, but given that this was supported by both sides of the aisle, it is expected to continue to stay in place, with perhaps some elements being repealed.

- Tariffs: The expected increased tariffs will make products more expensive, and given Trump’s 1st term is likely to be implemented through his executive orders. This will also have a secondary impact on driving on-shoring / near-shoring that will further increase in prices.

- Tax cuts: Bottom line is that this will increase household income and drive further demand based inflation.

- De-regulation: Lighter touch regulation with fewer antitrust cases and lesser scrutiny on MSA. Particular industries that are likely to benefit include the financial, energy, healthcare, and crypto industries. There is the possibility of a slowdown in the energy transition, and the US likely to leave the Paris Climate Agreement and re-focus on traditional energy sources.

- Tight labor market: Continued increases in non-farm payrolls suggest that demand for services will remain elevated, which will contribute to inflationary pressures. Unionized negotiations will fuel wage increases, but with the desire to reduce the size of the government, we have the potential of seeing some shifts in the employment market especially with the impact of AI.

The geopolitical environment has a lot of uncertainties especially with foreign relations. One expected outcome is likely to be funding cuts for Ukraine.

Conclusion

As inflation is on the rise again and with Trump winning the presidency combined with interest rate reductions Truflation continues to expect demand to accelerate and inflation to experience upward trajectory. Monitoring these factors will be essential for understanding the broader economic implications. The resilience of the economy, coupled with specific sector pressures, suggests a nuanced path ahead as policymakers navigate interest rates and other economic levers.

About Truflation

Truflation provides a set of independent inflation indexes drawing on 30+ data partners/sources and more than 14 million product prices across the US. These indexes are released daily, making it one of the most up-to-date and comprehensive inflation measurement tools in the world. Truflation has been leveraging this measurement tool to predict the BLS CPI number, with four predictions spot on and all but one deviating by no more than 20 basis points since coverage was initiated.

APPENDIX A

Truflation Category Percentage Change Data

Month-over-Month and Year-over-Year

All Data is based on October 2024

Truflation

Privacy Policy | © 2025. Truflation - All Rights Reserved.