BLS Housing Data Discrepancies & Adjusting Our Model: Truflation US Post BLS January Prediction Analysis

Published 02 Mar, 2023

As regular readers of Truflation’s updates will know, once per month we publish a forecast for US inflation. Separate to the Truflation index - which is an independent, verifiable and real-time measure of inflation - these forecasts seek to predict the inflation figure that the US Bureau for Labour and Statistics (BLS) publishes every month.

Frequently noted in the media, Truflation has been consistently on target with these predictions. Last month, however, we were out. While we predicted official annual US inflation to fall to 5.8% for January from 6.5% in December, it in fact held almost steady at 6.4%, down just a marginal 0.1% from the month previously.

To understand why our prediction was out, we have done a deep dive into the BLS data. From this, we are able to report that the housing sector is the culprit. Truflation’s housing index has shown a consistent fall in the rate of housing inflation since July 2022 and is supported by external data. The BLS has reported a continued rise over this time.

The outcome is that the BLS lags Truflation housing trends by nine months. This is a result of the BLS using rent as a proxy for owner costs, its flawed rental sampling methodology, and a lack of alternative data to predict owned housing costs. Below, we explain all of this in more detail.

WIDE RANGING FORECASTS

While this BLS inflation number did fall within the range of expected forecasts, this range was far wider than in previous readings, with predictions ranging from Ameriprise and Truflation’s 5.8% at the lower end and SMBC Nikko Securities and Kalshi’s 6.7% at the upper.

It is particularly concerning that the range of forecasts was so wide and that the views on the general direction of inflation were polar opposites. The only consistent view was that the MoM CPI percentage change would increase, which it did by 0.8% in the BLS estimate.

However, the majority of categories in the BLS estimate were broadly consistent with our own price change predictions. The only outlier was the housing category, where estimates were wildly different from other reputable industry sources whose data we rely on.

BLS VS TRUFLATION: THE WIDENING GAP

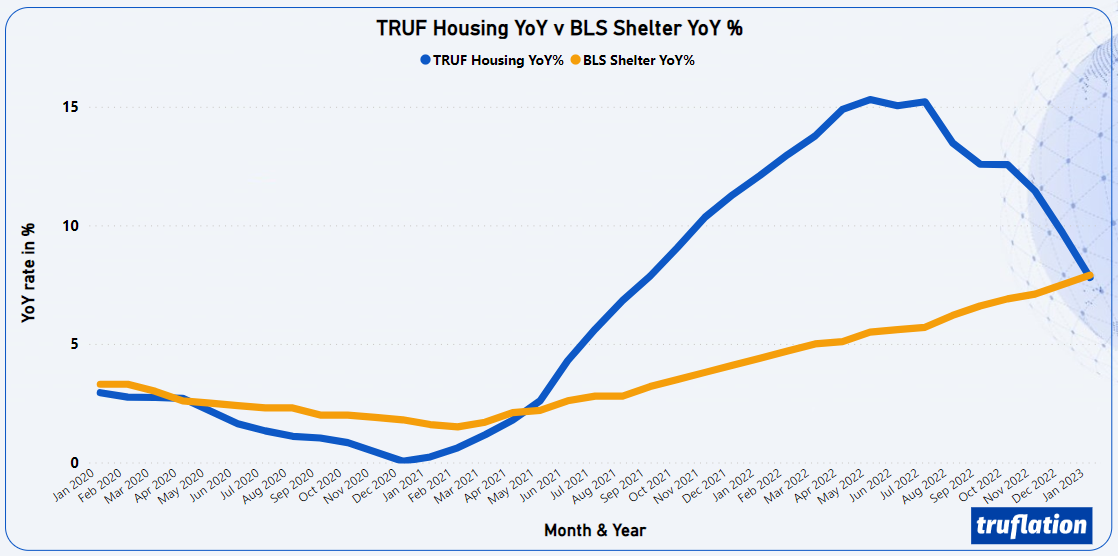

Throughout 2022, the gap between the BLS and Truflation housing price forecasts has been widening, as can be seen from the graphs below. The first graph shows YoY percentage change in the price of housing over the last three years.

Evidently, the BLS began to see price increases in the housing category in March 2021, which have continued unabated ever since. Truflation, on the other hand, saw housing pricing beginning to edge upwards three months earlier, a steeper rise, but then a marked drop from July 2022 onwards. The BLS never reported this drop.

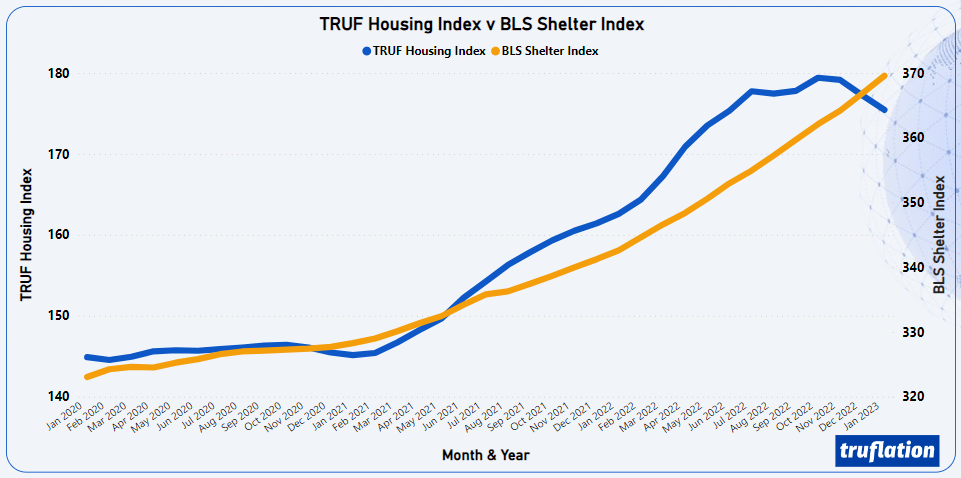

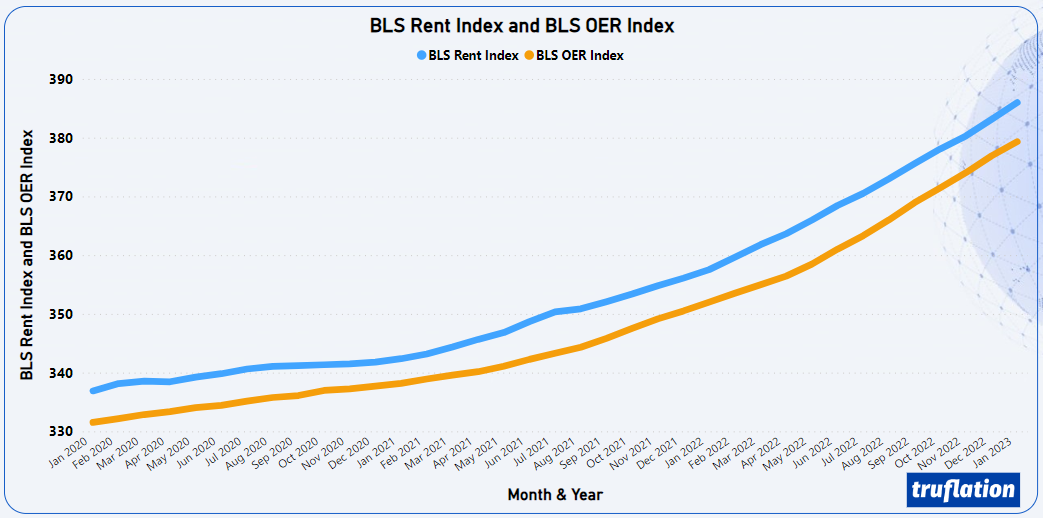

The second graph shows the same data on an index level. Like the previous chart, the BLS housing index looks unnaturally smooth, with no drop-off in July 2022, which is a trend reported by the majority of our data sources.

In fact, our analysis shows that the BLS housing inflation curve should be nearing its peak, which would put it nine months behind Truflation’s data. As such, we expect to begin seeing a drop in the BLS housing index in the coming two months.

THE DEFINITIONS OF HOUSING

Housing is a broad category and it’s important to understand its definition before digging into the specifics. Since housing makes up 34% of the overall CPI index as measured by the BLS, it is extremely important to calculate this metric correctly.

It is fair to say that measuring changes in the cost of housing is a more complex task than predicting price inflation for eggs or gasoline. Truflation uses data from 13 different sources for its prediction, with all data gathered in real-time. Having reviewed this data, we believe there is a significant lag between the rate of housing inflation reported by the BLS (“shelter” in the BLS release) and the actual price changes in this category.

THE BLS HOUSING MEASUREMENT

The BLS has a particular way of calculating the costs of housing, or “shelter”, which is different from other sources. Firstly, it considers rent and housing costs to be one and the same. In other words, it assumes that homeowners will be paying an equivalent amount in mortgage as renters would pay for the same property, adjusted for size and location. The only difference is that for homeowners, this figure strips out utilities. The utility costs of rental properties are also included if they are part of the rent paid by the tenant. This is known as the Owner’s Equivalent Rent (OER).

With this method, the BLS intends to measure the cost of the consumption value of a home, rather than the changes in value of a house or the actual monthly mortgage repayments. This method has obvious flaws, since there are likely to be a significant number of homeowners who have paid off a portion of their mortgages. For these individuals, the costs would be lower than for property renters.

Meanwhile, when it comes to tenant rent, the BLS includes any government subsidies paid to the landlord in the total cost of the rent, which is also likely to skew the data to the upside. The BLS does take some measures to keep its sample representative, however. It adjusts for the quality of the properties it observes based on age, neighborhood improvements and physical renovations to the home, and it replaces one-sixth of the sample each year.

Yet this is not enough to dispel our concerns, which also include the sample size and the frequency of its collection. The BLS collects data on rent for only around 50,000 residences through personal visits or telephone calls and each individual unit is only sampled every six months. Considering that around 35% of US households are rented, this seems a small sample to draw such an important statistic, and taken only twice yearly.

THE FLAWS IN THE BLS MEASUREMENT: WHY OER IS NOT A SUITABLE METRIC

Using the OER as a metric to bring owner-occupied housing and rental properties under the same umbrella has many pitfalls. Firstly, finding rental housing that is comparable to an owner-occupied unit is difficult.

Predominantly, renter-occupied neighborhoods are often geographically separate from owner-occupied ones (a city center versus a suburb). Even in the same neighborhood, the former could be multi-family buildings, while the latter are often single-family homes, for example. This, coupled with the difficulty in finding comparable quality of housing, adds a significant complexity to the BLS measurement that puts the consistency and validity of the numbers into question.

In addition, methodologies for measuring owned property prices are not foolproof, as it is not an easy task. As such, using a mix of methods and data sources, which is the approach taken by Truflation, is sure to deliver more accurate results than relying on OER alone.

TRUFLATION’S HOUSING MEASUREMENT

In contrast, when calculating the Truflation housing index, we include a combination of rental prices, household debt, and property prices, drawn from 13 independent sources. Housing makes up 23% of the overall Truflation CPI index versus 34% of the BLS category.

For rental price data, we use seven data sources that monitor a combined 4 million of transactions per month, including Zillow, Trulio, Redfin, Apartment List and CoreLogic. For owned properties, we source data from five sources, including the New York Fed Reserve, Redfin and CoreLogic.

Our methodology for calculating rental price changes incorporates both new rental agreements and rental renewals, which provides us with a balanced view of price changes over time. In addition, the data for owner-occupied properties covers both property value changes and the changes in the household mortgage debt.

Truflation’s model ensures that we cover the whole spectrum of the housing market. Well-known rental data indexes, such as the one published by Zillow, capture the rents of units currently advertised, but don’t include continuing renters. We ensure that we include data from other sources to plug this gap.

TRUFLATION VS BLS: A LIKE FOR LIKE COMPARISON

In order to compare the Truflation and BLS models like-for-like, we have dived both housing categories into the following sub-categories:

1. Rent of primary residences

2. Lodging away from home

3. Owners equality of rent of residences

4. Tenants and household insurance

The table below shows the relative importance of each of these subcategories to the BLS and Truflation housing indexes, respectively.

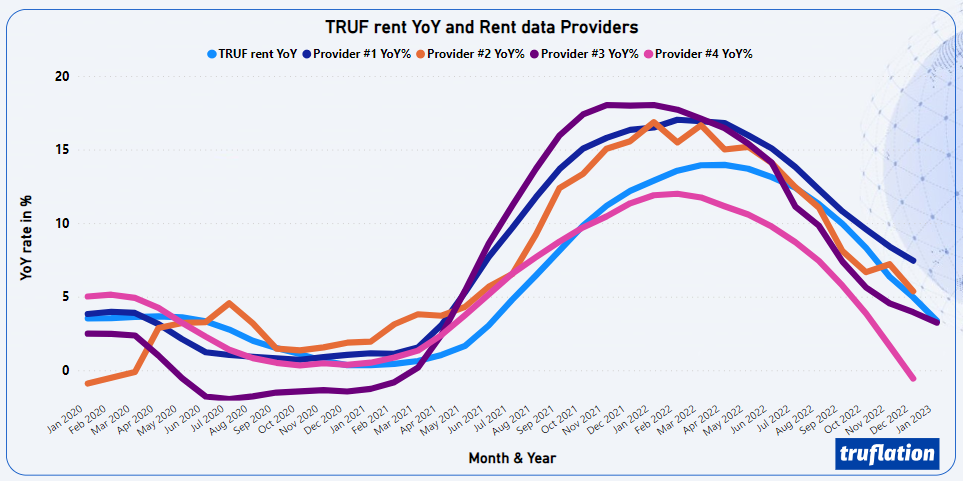

BLS VS TRUFLATION: RENTED HOUSING

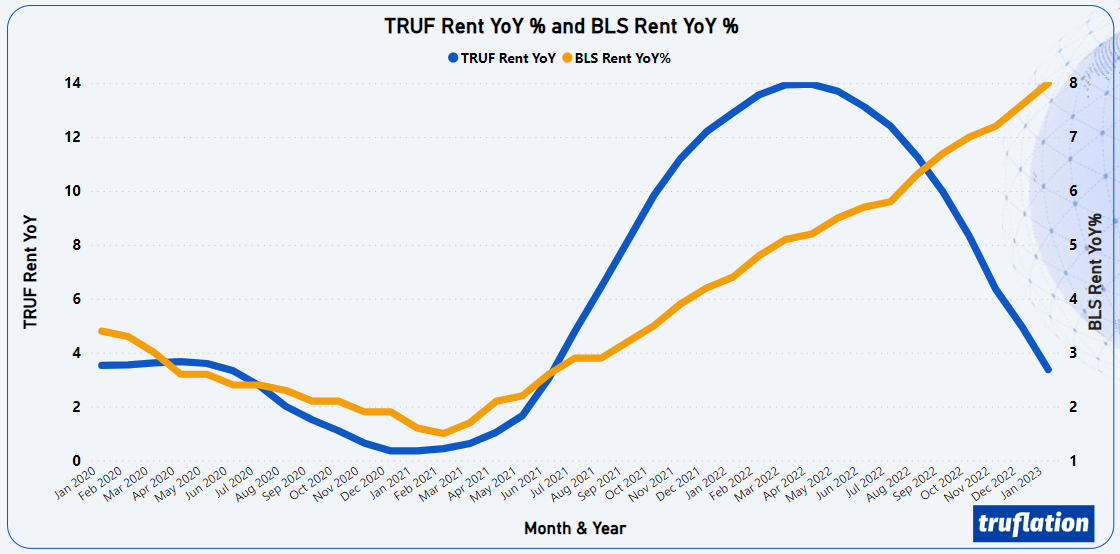

Digging deeper into rented housing data, it is clear that BLS suffers from the same problem in this sub-category as the overall index itself. Both the YoY and MoM indexes are very smooth and don’t reflect the cooling of the rental market that has been evident from other data sources over the past seven months (see graphs below).

The third graph clearly shows this downward trend in rental prices based on data from five reputable data sources that we use for our housing price estimates. Since some 34% of all households in the US are rented, this trend should contribute significantly to the overall housing price chart.

For example, CoreLogic shows single-family rental price increases dropping to 7.5% YoY in November, which marked the seventh consecutive month of annual deceleration. CoreLogic expects that rental price growth, along with home price appreciation, will continue to level off during the first part of 2023. This is consistent with Truflation data, but the opposite of what the BLS is reporting.

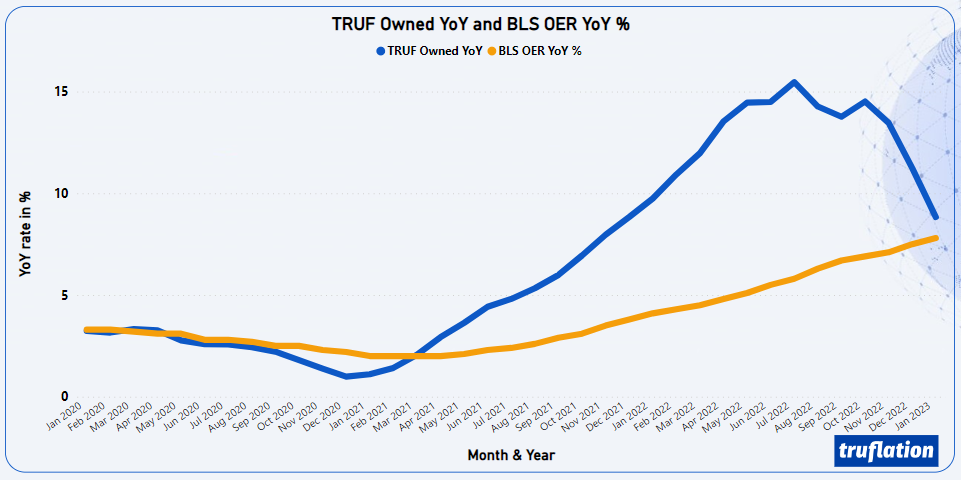

BLS VS TRUFLATION: OWNER-OCCUPIED HOUSING

A comparison of the BLS and Truflation owner-occupied housing price graphs shows the same trend as rental properties, as evident from the graphs below. In fact, the MoM and YoY owner-occupied housing lines look almost identical to the BLS rental price index.

While Truflation’s YoY index peaked six months ago, the BLS index hasn’t even started to see a slowdown yet. As such, we believe that both rental price data and owner-occupied price data coming from the BLS is not an accurate representation of current housing price trends.

In addition, while house prices and rental prices are determined by supply and demand factors that generally move in tandem, house prices and rents themselves typically do not. If demand for home ownership rises because mortgage rates fall, for example, in the short term house prices will rise but rents won't. However, as the contracts come up for renewal, these prices will increase over time, typically with a long lag.

CONCLUSION: IMPACT ON TRUFLATION’S MODEL

Based on historical analysis, Truflation has been able to calculate the delay between real house price growth and OER inflation – the measurement used by the BLS. Our data shows that the correlation between these two metrics peaks at a nine-month delay, meaning that BLS housing data is nine months behind the real-time costs in this category.

To reflect this, we have adjusted the Truflation model accordingly. However, even taking this nine-month lag into account, the CPI estimate for January 2023 should have been 6.2%, instead of the 6.4% reported by the BLS.

Such discrepancies in the data are alarming. Especially in the current economic environment, inflation data has a material impact on the central bank’s monetary policy. A higher CPI reading could cause the US central bank to continue tightening its monetary policy in the erroneous belief that the economy is running hotter than it actually is. It may by time for the BLS to readjust its statistical assessments to ensure its data on a sector as important as housing is accurate and timely.

About Truflation

Truflation provides a set of independent inflation indexes drawing on 30+ different data partners / sources and more than 12 million product prices across the country. The indexes are released daily, making it one of the most up-to-date and comprehensive inflation measurement tools in the world.

Truflation has been leveraging its measurement system to predict the BLS CPI number. In the last three months, Truflation’s predictions have been spot on for two months and 20 basis points off for the third, highlighting its strength as a measurement tool combined with a comprehensive model to predict the CPI number.

Join the Truflation Community

Telegram

Discord